Chapter 14: Social Security Administration

Social Security Administration (SSA) is one of the smaller services, accounting for approximately 1.7% of total public service productivity expenditure. It covers the administration of benefits to individuals and households including Universal Credit, Housing Benefits and more.

In the UK in financial year ending 2023 around 87% of expenditure on SSA was spent by the Department of Work and Pensions (DWP), with the residual being the responsibility of either a) HM Revenue and Customs (HMRC) in relation to the administration of Tax Credits and Child Benefit, noting that the process of migration of Tax Credit recipients to Universal Credit has been continuing for some time, or b) top tier local authorities in relation to the administration of Housing Benefit.

Historically, Atkinson (2005) and subsequent Office for National Statistics (ONS) research made progress in delivering a direct measure of SSA output, driven by the number of case-files being processed, or maintained on the caseload, but without any quality adjustment. As described in Chapter 3, the value of the benefits themselves is considered a transfer and is not a direct measure of output. This measure, however, was a partial and incomplete solution.

Further to this, the historical methodology was suspended in 2018 following the introduction of Universal Credit, which caused significant methodological issues to arise given its rationalisation of various benefits into one. The existing measure, whilst strong in terms of technical efficiency (e.g. reducing the costs of processing each type of existing case-file), was insufficient to address allocative efficiency (e.g. the merger of various types of benefit into a single case file).

14.1 Prioritisation of issues

The Review prioritised resolving immediate issues relating to the introduction of Universal Credit and the coronavirus (COVID-19) pandemic, rather than longer-term challenges relating to the measurement of Tax Credits and Child Benefit. As a result, the measures developed focus on DWP activity, covering output from 2013 (upon development of the output model to account for Universal Credit) and quality adjusted output from 2008. The Review also investigated DWP and HMRC inputs pre-2013 to gain an understanding behind historic volatility, however no methodological changes were implemented from this.

The in-depth analysis of input and output data of the Review (back to 1997 and 2013, respectively), however, indicates that expenditure on Tax Credits and Child Benefit administration by HMRC is not separately identifiable within data returned via the HM Treasury Online System for Central Accounting and Reporting (OSCAR) system, potentially recorded as costs of General Public Services (COFOG 1), which are not included in the SSA classification.

As a result, administrative costs for Tax Credits and Child Benefit are likely not being accounted for in the SSA inputs model. Therefore, the ONS do not include the output measures of Tax Credit in the calculation of SSA. Including this information in the outputs, but not the inputs could lead to misleading changes in productivity estimates. The Review believes that the DWP share of SSA has been historically over-stated as the large amount of HMRC Tax Credits have not been included, which suggests the historical method applied may have been subject to bias.

As a priority, the Review has developed a new method, working closely with DWP and HMRC, that better captures the administrative activity in the transition from legacy benefits to Universal Credit, particularly from 2018.

The new measure addresses the challenge of addressing allocative efficiency, but this means that comparisons between the existing measure and the new one are relatively challenging to make and interpret. Previously compositional changes in the caseload demographics may appear erroneously as productivity movements, although this remains the case for those elements which remain cost weighted.

However, this improved methodology currently only captures DWP activity whilst inputs and outputs data on Tax Credits and Child Benefit cannot be sourced. Equally, the Review has not had the resources to explore local authority data on Housing Benefit inputs and outputs.

The data which the ONS will release in the Spring 2025 statistical bulletin will therefore focus on DWP activity but are expected to be liable to substantive revision, particularly as Tax Credit information is brought into the calculation (importantly, in terms of both inputs and outputs), which is likely to change the relative weights of DWP and HMRC activity within this series, particularly historically. These data should therefore be considered as ‘Official statistics in development’. Once this has undergone further testing, it will become an ‘Accredited official statistic’ in line with the rest of the estimates.

The Coronavirus Job Retention Scheme was launched in April 2020 and aimed to protect jobs affected by the coronavirus pandemic. This is not currently considered as part of the SSA services and expenditure is therefore recorded within the “Other” grouping. Further consideration of this matter is advised.

Recommendation 100:

The ONS should undertake further work to identify the best treatment of the Coronavirus Job Retention Scheme.

This development of the output measure of SSA is supplemented by a new quality adjustment reflecting DWP Fraud & Error. Again, HMRC expenditure and performance data on Fraud and Error related to Tax Credits should also feed into this metric, as well as wider measures of quality across the SSA service. The partial coverage of the quality adjustment means this should be considered ‘experimental’ until further notice.

Finally, the Review has introduced an improved intermediate consumption deflator in line with the UK National Accounts development, impacting slightly on inputs. These improvements will be incorporated into the upcoming annual publication in Spring 2025.

14.2 Methodological and data challenges addressed by this Review

Setting aside the longer-term issues related to accessing data on Tax Credits, Child Benefit and Housing Benefit addressed at the start of this chapter, the major methodological issue tackled by the Review was the introduction of Universal Credit to rationalise numerous legacy benefits into one, which was exacerbated by the impact of the coronavirus pandemic.

The three main challenges considered by the Review can be summarised as:

- Inputs volatility: SSA inputs show considerable volatility over time, more so than other services. The ONS explored the data sources and systems to assess the main drivers of these movements to determine their legitimacy, and if any methodological changes need to be considered.

- Output: Developing a method to appropriately treat the transition from multiple legacy benefits into one single benefit (Universal Credit) while considering conceptual implications around the capture of technical versus allocative efficiencies, and updating the methods used for those benefits which have not been replaced by Universal Credit. This has an obvious implication that there is a need to also review those benefits not impacted by the change to ensure wider consistency.

- Quality Adjustment: Consideration of outcomes such as fraud and error, customer satisfaction and timeliness to better capture the quality in the delivery of benefits to recipients. The rationalisation of numerous benefits into Universal Credit presented an opportunity to improve the productivity of benefit delivery. However, under the traditional cost weighted method the relative values assigned to Universal Credit and its legacy benefits would have been based on their cost, so in the absence of commensurate cost savings, this scheme would have weakened, instead of strengthened, productivity estimates. As described in previous chapters, this is an example where existing methods failed to suitably address allocative efficiency improvements. Methods revisions in a number of services have, under the Review, been undertaken with a view of ‘future-proofing’ methods against this risk re-occurring.

The existing methodology was therefore judged to be severely limiting in the light of the development of Universal Credit, and prior to the coronavirus pandemic, the ONS suspended publication of SSA’s direct measure of output. Though the intention was to rapidly develop an alternative improved methodology to deal with the transition, the emergence of the coronavirus pandemic shifted resource away from doing so, until the launch of this Review. In the meantime, the “inputs = outputs” convention was applied from 2018 onwards and, as a result, SSA productivity has been constant since.

14.3 Improvements to inputs estimates

The methods applied by the ONS to estimates SSA inputs have not changed since the Atkinson Review. This method is based on deflated national accounts data (including compensation of employees, intermediate consumption, and consumption of capital) for activity in the relevant service (which in this case is COFOG 10 – Social Protection).

The inputs data were reviewed in detail to understand the key drivers of volatility in the back-series. The Review investigated the compilation of the national accounts’ COFOG 10: Social Protection data back to 1997 (when the series began) and corroborated that with HM Treasury’s OSCAR database back to its starting point in 2012 to 2013.

Summary of SSA inputs volatility

The SSA inputs index begins in 1997 and year-on-year volatility is most evident between 2003 and 2013. The index’s annual average growth rate in absolute terms before this period is 6%, during this period it is 13%, and after this period it is 4%. Further interrogation of the data showed that trends in intermediate consumption were driving the volatile movements in the inputs index, as opposed to labour or capital consumption.

Although a large increase was observed for local government intermediate consumption expenditure in 2008, it was clear that most of the volatility stemmed from central government intermediate consumption expenditure. It particularly drives movements in the following periods:

- 2003: coinciding with the introduction of pension credit, the Income Tax (Earnings and Pension) Act, and establishment of Jobcentre Plus.

- 2007 to 2013: coinciding with changes to the demand in claims for benefits such as Job Seekers’ Allowance.

- 2013 to 2015: coinciding with increased expenditure on ‘Clinical & Medical’ spend in OSCAR, which rose in accordance with an increase in Disability Living Allowance (DLA) claims, and the need for additional resources to meet the demand of assessing claimants’ health conditions and thus eligibility for DLA.

Local government intermediate consumption also adds to some of the volatility, rising sharply in 2008. This reflects the average rise of £9 a week for Housing Benefit claims, which led to increased administration costs (+£0.2billion). There was also a £0.7 billion increase associated with concessionary transport fares, coinciding with the extension of the English National Concessionary Travel Scheme to free off-peak national travel from 1 April 2008.

However, it is uncertain whether these costs are solely attributable to administrative burden (see Recommendations for future work) or may contain some element of the value of the benefit or subsidy for concessionary schemes. Whilst recognising these are small, given these components are not costs of the administration of these benefits, but rather the benefit themselves, this may merit further investigation.

Recommendation 101:

The ONS should review whether data exists to better understand, for Social Security Administration, whether non-administrative costs for concessionary fares and Housing Benefit are correctly recorded, and whether they are sufficiently impactful to merit further work.

Verifying data sources

Investigations were conducted into the compilation of UK National Accounts data to ascertain whether inputs movements from 1997 onwards are attributable to actual DWP spending data, or adjustments that are applied to the data by the ONS. More than two-thirds of the data feeding into SSA intermediate consumption, of which most of the volatility stems from, is actual DWP expenditure from the OSCAR dataset. The remaining third is made up of other data, including adjustments.

These adjustments are applied for reasons such as error correction, redistribution of quarterly expenditure across a financial year, or re-allocation of expenditure (e.g. allocating some defence expenditure to healthcare). In all cases, adjustments are agreed and implemented as part of a collaborative exercise with HM Treasury on an annual basis.

Nevertheless, the adjustments account for a similar amount of volatility as the DWP data, despite having a much smaller share of contribution to intermediate consumption levels. The Review has investigated this and overall, is confident in the legitimacy of SSA inputs. The movements reflect changes in social security over time, they are predominantly driven by DWP-reported accounting, and the adjustments resolve clear oddities, such as in 2005 when the raw data appears unfeasibly low.

COFOG structure

The Review also investigated the COFOG structure within SSA, noting that it should cover benefits administered by DWP alongside Housing Benefit which is administered by local authorities and Tax Credits and Child Benefit, both of which are administered by HMRC. These non-DWP components, the Review has concluded, may be excluded from either or both inputs and outputs and therefore this appears to be an area for further improvement, as noted in Recommendation 95. Given this, the time series appears a valid estimate of those DWP services currently in-scope of the data collection, but in time should change from being DWP-focussed to SSA-focussed as data improves.

14.4 Improvements to outputs estimates

The ONS SSA output measure used data from DWP for benefits administration in Great Britain until 2018 when the previous measure ceased to be produced and the “inputs = outputs” convention was used due to the complexities in relation to the implementation of Universal Credit, specifically:

- The replacement of multiple “legacy” benefit schemes by Universal Credit.

- The changing composition of Universal Credit claims over time, as the transfer from legacy benefits to Universal Credit started with the simplest cases, with progressively more complex benefit claims transferred over time.

The first of these issues prevented the measurement of any productivity change resulting from the transfer to Universal Credit. If Universal Credit could deliver equivalent benefits at lower cost, then a conventional index, using cost weights, would place a lower value on the new Universal Credit activity, and any resultant fall in inputs would be matched by a fall in output, and productivity would not change. This is clearly incorrect: delivering the same benefits or support to citizens at a lower administrative cost should be seen as a productivity enhancement.

For the second issue, the application of a conventional index, using cost weights, may result in productivity appearing to fall as a result of more complex claims having a higher cost of processing, but no greater value in output.

Introducing use of benefit weighting as an alternative to cost weighting.

The new output measure developed by the Review therefore involves:

- Producing a benefit-weighted index for the administration output of Universal Credit and legacy benefits, where the changes in the number of claimants of each benefit are weighted by their average benefit payments.

- Producing a cost weighted index for the remaining benefits, which uses an update to the existing claims and load activity data and associated unit costs.

- Producing an overall index for SSA output by weighting together the two indices described in the bullets discussed using the total administrative expenditure on all benefits within each index.

Using a stylised example of benefit weighting, a benefit payment bundle of equivalent value from Universal Credit and legacy benefits would be given equivalent weight in output and so output would not change where a benefit claimant was given equivalent support under legacy and Universal Credit payment schemes.

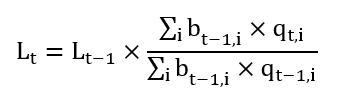

This means that where there is a difference in the cost of delivering equivalent benefits under the legacy and Universal Credit schemes, this will manifest as a change in inputs but not output. Therefore, the productivity measure will account for changes in the cost of delivery resulting from the introduction of Universal Credit. This is an over-simplification, used to illustrate the theoretical approach. In reality, the legacy and Universal Credit systems are not always directly equivalent. The formula for the Benefit Weighted Activity Index is as follows:

Figure 7

Where:

L = index

b = unit benefits (analogous to a unit cost, but weighting for benefits)

q = quantity of activity

t = time period

i = activity type

Recommendation 102:

The ONS should measure the output of the administration of Universal Credit and its predecessor legacy benefits using a benefit-weighted index to account for the allocative efficiency of the transition. This measure should be seen as provisional whilst undergoing further testing.

The legacy benefits included in the benefit weighted activity index include Employment and Support Allowance, Income Support, Jobseeker’s Allowance and Housing Benefit. Tax Credits, which were administered by HMRC, are not included as the inputs used to process these are not accounted for in the SSA inputs measure due to challenges in isolating these inputs from other HMRC activity. The Review therefore excluded Tax Credits from the SSA output measure and the ONS intends to continue investigating the appropriate data sources for Tax Credits in future.

Recommendation 103:

The ONS should seek to acquire data to incorporate Tax Credits, Housing Benefit and Child Benefit in both output and inputs measures of Social Security Administration, while making appropriate adjustments to the “Other” grouping of inputs.

In terms of accounting for changes in the composition of claims in Universal Credit, the increase in the number of entitlements per household over time represents an increase in the administrative output of Universal Credit. The challenge is that the calculation needs to account for the changing composition of Universal Credit claimants in output.

This means it is inappropriate to treat the administration of the average Universal Credit claim as having an equal value over time. Activity for Universal Credit should therefore be the number of Universal Credit claimants (households) adjusted for the change in composition and therefore assumed administrative burden of these cases. In the absence of evidence on the relationship between claimant composition and administrative cost the method assumes a relationship between these using the benefit award amounts to approximate their value.

Recommendation 104:

The ONS should adjust the output of Universal Credit administration for changes in the number of entitlements included in payments, to account for the heterogeneity of cases.

These changes are planned for incorporation into the ONS Spring 2025 annual statistical release. The ONS will account for the changes in composition of Universal Credit claims by applying a composition adjustment to the activity for Universal Credit. This estimates changes in the composition of Universal Credit claims and therefore processing of Universal Credit payments, while controlling for uprating of Universal Credit payments over time to account for inflation. Detail is provided in Annex G.

Although Universal Credit was introduced in the financial year ending 2014, the existing SSA output index for the period 2013 to 2016 did not include Universal Credit. It should be noted the significant increases in compositional change to Universal Credit claims came into place post-2016, which along with the large-scale roll-out of Universal Credit coming after 2016, means the absence of a composition adjustment factor before 2016 should have a limited effect on output over this period.

However, activity and unit cost data provided by DWP has enabled the ONS to calculate a conventional cost weighted activity index including Universal Credit for the period financial years ending 2014 to 2017. Claims and load for Universal Credit activity is therefore included in the index for this period in the new measure but is not adjusted for compositional changes. Given feedback to the Review suggests the easiest cases were moved to Universal Credit first, failure to weight-up more complex cases in this period should have less impact. This cost weighted activity index is then combined with the existing SSA output index for 1997 to financial year ending 2014 by retaining the growth rates for this earlier period and applying the growth rates from the new approach for financial year ending 2014 onwards.

For the benefits that are not Universal Credit or its legacy counterparts, a simple cost weighted activity index will continue to be used post-2016. This will retain wider comparability with other services, which continue to use cost weighting.

14.5 Improvements to quality adjustments

There are currently no quality adjustments in SSA productivity estimates. The Review explored several possibilities, namely use of a) DWP fraud & error rates, b) customer satisfaction surveys, and c) timeliness of processing claims. The Review concluded that only the first of these was suitable for implementation at this time.

Fraud and error rates

The methodology has been prepared to incorporate fraud and error indices for benefits administered by DWP, and those administered by HMRC such as Tax Credits and Child Benefit. These are planned for implementation in published statistics from the Spring 2025 ONS annual release, however as HMRC outputs will not be included in the SSA output measure, fraud and error rates for DWP only will be included.

Existing annual National Statistics report DWP’s stock of Monetary Value of Fraud and Error (MVFE) by benefit and by cause. Much of the quantifiable DWP administration activity has been focussed on enhancing the outflow from the MVFE stock by detecting and correcting erroneous benefit payments. This activity is quantified through targets reported to HM Treasury as delivering Annually Managed Expenditure (AME) savings (financial year ending 2025 target £1.7 billion).

However, a focus of AME savings can create perverse incentives, when the goal should be to prevent the inflow of inaccurate benefit payments at source into the MVFE stock. Those preventative safeguards require investment to verify and block expenditure in which the value for money impacts are difficult to measure. Additionally, a rising propensity for fraud in society (and accepted within Office for Budget Responsibility forecasts), recognise a system not in steady state where additional administration is required just to maintain current levels. See Annex G for more detail.

In addition, these stock measures of fraud and error may not reflect the flow of new fraud and error cases which are a more accurate measure of in-year delivery.

Recommendation 105:

The ONS should apply a quality adjustment in Spring 2025 based on existing Department of Work and Pensions fraud and error rates.

Recommendation 106:

The ONS should work with the Department of Work and Pensions to replace stock measures of fraud and error with more appropriate flow measures to better reflect in-period performance, in Social Security Administration quality adjustment.

Customer satisfaction

Claimants’ views on the effectiveness of the claims process can reveal helpful insights into the quality of a service. The Review explored the potential of using the DWP and HMRC customer surveys. Whilst, in the DWP survey, results cannot be compared before and after 2013, and there were further methods revisions in 2020, this remains an otherwise prime potential data source, although the Review notes the need for comparable HMRC data for completeness. More information is provided in the Recommendations for further work section.

Timeliness

The time taken for claimants to receive benefits can drastically affect their ability to manage their finances effectively. The Review therefore explored the potential of using timeliness metrics related to benefits administered by DWP and HMRC. However, there are complexities in relation to the different time periods permitted for simple and complex cases or various eligibility checks which means the Review could not recommend proceeding with this metric at this time. Further investigation may however be merited.

14.6 Devolved governments

The ONS does not include benefits in Northern Ireland which are administered by the Department for Communities, although the Review recommends further investigation into data sources for including benefits in Northern Ireland in future.

Recommendation 107:

The ONS should investigate data availability accounting for benefit administration in Northern Ireland, as the current measure does not include that activity.

14.7 Recommendations for further work

Inputs

Administrative costs associated with benefits delivery are being captured within SSA inputs, however there is a question on whether only administrative costs are being captured for administration of concessionary travel fares, which are governed by local government, or whether the costs for concessionary fares are included, which would be erroneous.

Recommendation 108:

The ONS should further investigate whether administrative costs associated with benefits delivery are being captured in Social Security Administration.

Quality adjustment

Customer satisfaction

Two approaches could be considered in the area of customer satisfaction:

- Utilising departmental customer surveys: DWP’s Customer Experience Survey appears a strong data source, although the Review would encourage the ONS to work with DWP to consider potential improvements and collaborate on obtaining a consistent long-term time series. For example survey questions could be re-worded to obtain participants’ perceptions exclusively on their experiences with Tax Credits or Child Benefit, which would avoid the challenges of merging two surveys, one from HMRC and one from DWP.

- Utilisation of the OPN: The ONS’ Opinions and Lifestyle Survey (OPN) has the potential to provide consistent insight into public satisfaction of multiple public services, but obviously with far less depth. This however may act as a helpful means of triangulating and validating movements in the DWP and HMRC data. The OPN, it has to be noted, only covers Great Britain, therefore the Review would recommend augmentation with Northern Ireland’s Omnibus Survey and Continuous Household Survey for complete UK coverage.

Recommendation 109:

The ONS should continue to work to identify the most appropriate route to capture user satisfaction in Social Security Administration across the UK.

Timeliness

There is potential to improve existing timeliness data, including potential new data sources, such as the Operational Performance Research Analysis (OPRA) which aims to amalgamate timeliness measures from all benefits administered by DWP into a single metric for the inclusion in their annual reports and accounts.

Another consideration could be to identify the numbers of claims being processed in relation to actual claims administered to produce a proxy waiting list. The median processing time for benefits may also be explored.

Recommendation 110:

The ONS should continue to collaborate with the Department of Work and Pensions to develop data on timeliness for Social Security Administration.

Weighting

Having a single quality adjustment avoids the question of how to weight together disparate measures in the short-term, but clearly remains a potential issue if others are developed. Surveying taxpayers on the relative importance of the three quality adjustments may present the simplest way to determine a weighting mechanism. The existence of the DWP Customer Experience Survey, with subtle methodological improvements, could meet this need. Relative spend on delivering fraud and error, timeliness or customer facing activities would deliver an alternative. A third option could be any inspection regimes which have received Ministerial sign-off.

Recommendation 111:

Weighting mechanisms for baskets of quality adjustment factors, such as in Social Security Administration, should be considered and if necessary, data collected to ensure quality adjustment estimates reflect societal preferences and that these are aligned with how other relevant areas are treated, such as health waiting lists.